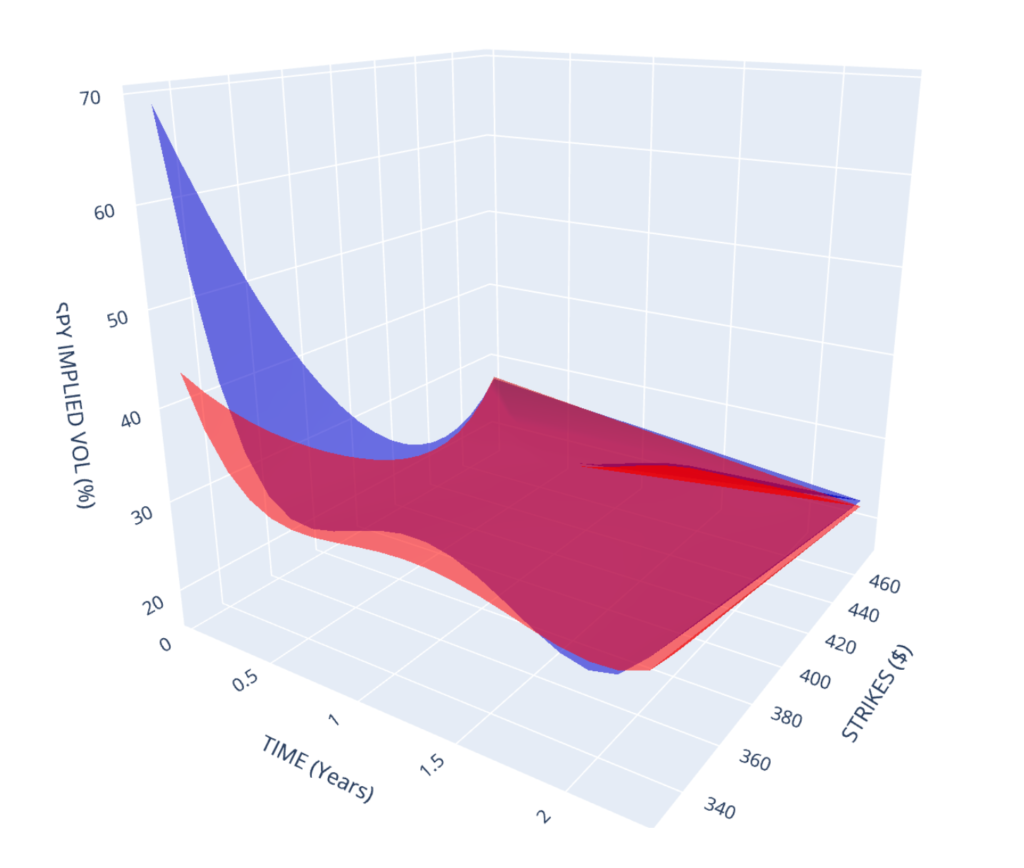

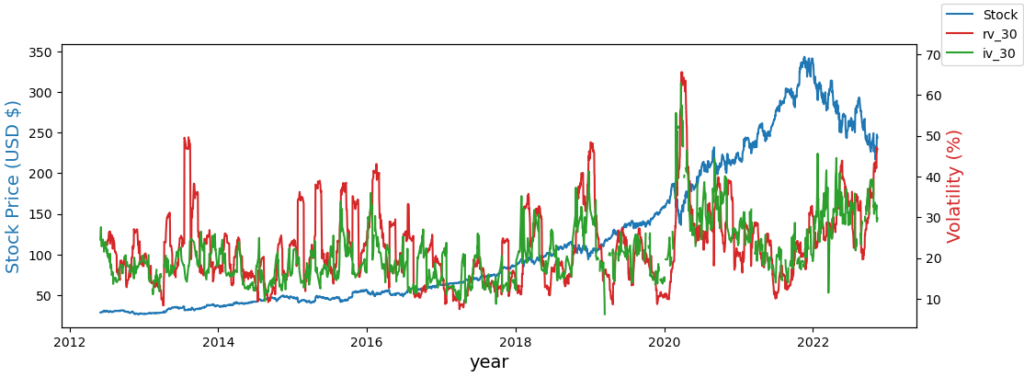

Implied Volatility vs Historical Volatility

In today’s tutorial we investigate how you can use ThetaData’s API to retreive 10 years of historical options data for comparing Implied Volatility to Historical Volatility. We also describe what the difference between historical volatility and implied volatility actually is.