Simulated Stock Portolio

In this tutorial we will implement the Monte Carlo Method to simulate a stock portfolio over time.

In this tutorial we will implement the Monte Carlo Method to simulate a stock portfolio over time.

There is an extremely high false discovery rate in both the academic and financial industry for trading strategies that “produce” alpha. In fact, most of these strategies are false discoveries due to research bias, multiple testing and the true probability of finding a new investment strategy being very low (<< 1%) due to competition. Today we investigate issues of multiple testing and false discovery of a profitable trading strategy. We develop a momentum-based trading strategy on Apple stock and show the issues that can arise from unknowingly completing multiple testing on the same dataset.

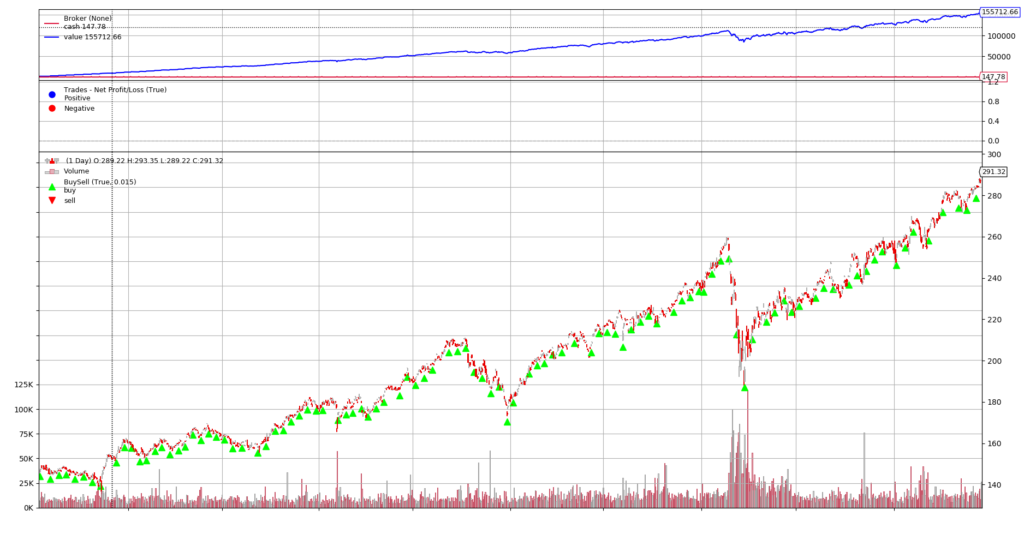

Here we will be using BackTrading as a back testing framework to evaluate the difference between dollar cost averaging strategy and lump-sum investing.

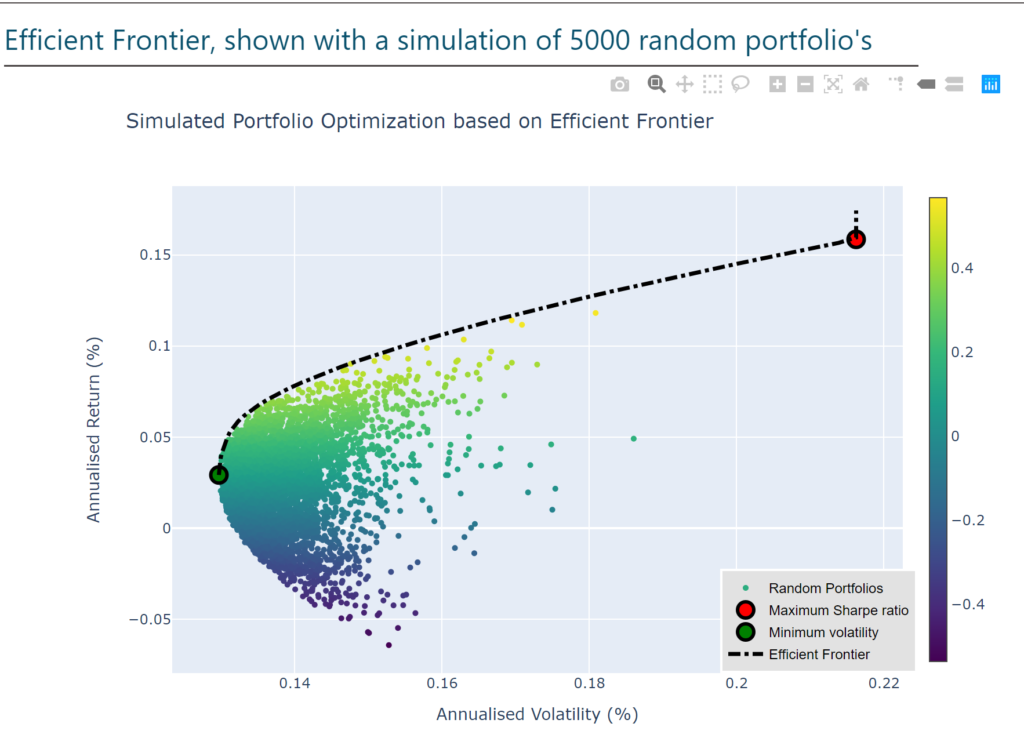

The Efficient Frontier is a common phrase in Modern Finance since the inception of Modern Portfolio Theory in 1952 by Harry Markowitz. Here we learn how to complete portfolio optimisation using the Markowitz’ approach to find both minimum variance and max sharpe ratio portfolio.

In this tutorial we aim to use the key indicators that Warren Buffett uses to determine the strength of an underlying business, so that we can find excellent stocks that are worth more time investigating. However the ASX alone currently has 2061 listed stocks, how can we possibly reduce that number? With our Quant hat on, we can expedite this process using some key assumptions and our skills in python.

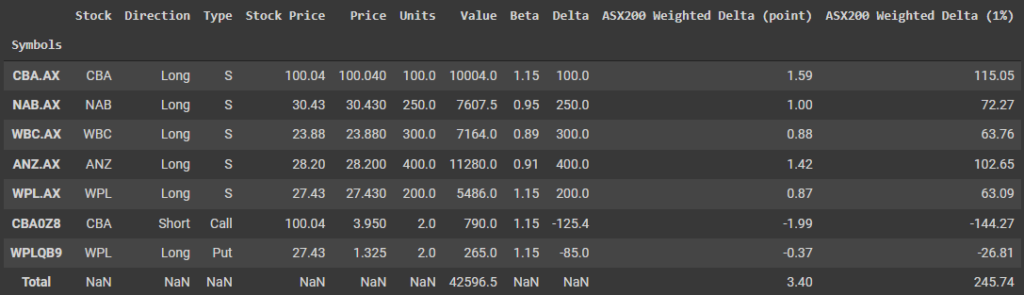

Beta weighting is a tool that allows us to approximate our positions in terms of the same benchmark. Today we learn how to beta weight your portfolio in python.

We will use three equivalent methods to estimate the beta coefficients of each security and then progress onto how you can beta weight your portfolio delta’s (the change in value given a unit change of the underlying) to get an approximation for how your portfolio will change with respect to a movement in your benchmark (whether it be a market index or specific security).

In this tutorial we compute and track historical volatility over time. We also explore how to calculate trailing historical finanical metrics like Sharpe, Sortino, Modigliani and Calmer ratio. Along with the calculate of overall max drawdown.

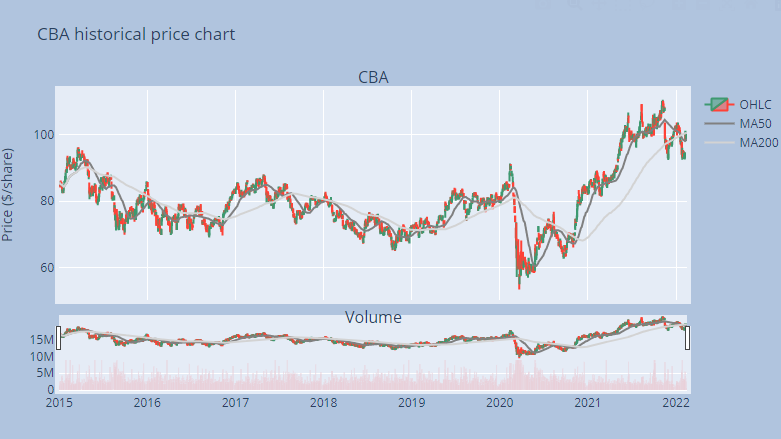

Learn how to use pandas dataframe and plotly to create a historical price and volume stock chart.

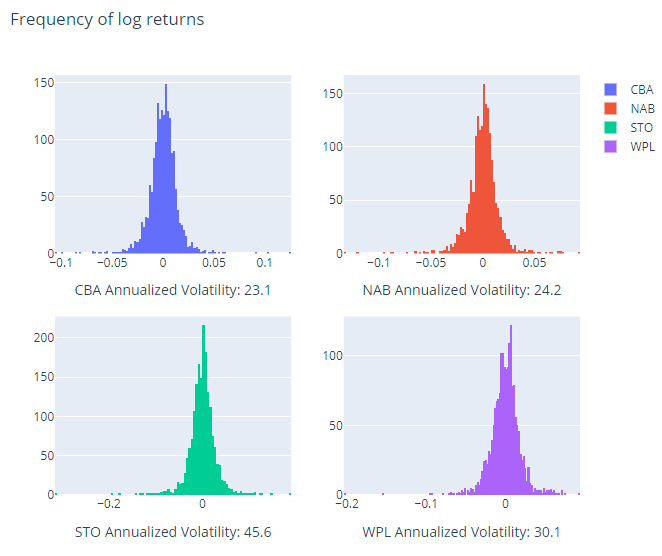

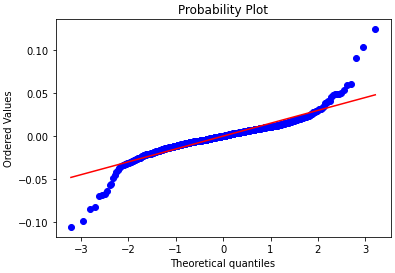

In this tutorial we try to understand the difference between simple returns and log returns.

We also talk about normality of financial data, and how to perform statistical tests to test for normality.