Beta Weighting your Portfolio

Beta weighting is a tool that allows us to approximate our positions in terms of the same benchmark. Today we learn how to beta weight your portfolio in python.

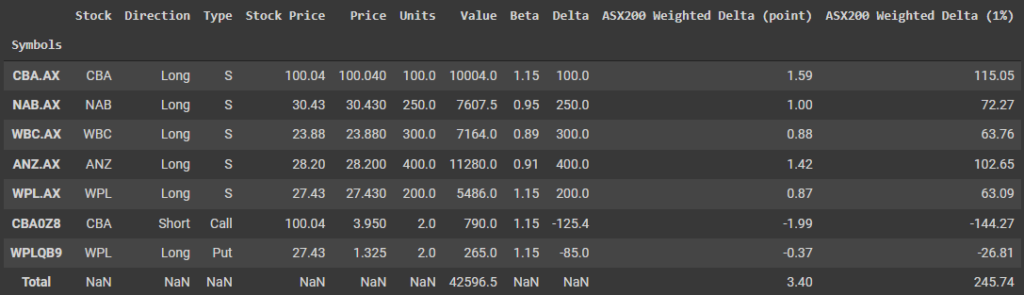

We will use three equivalent methods to estimate the beta coefficients of each security and then progress onto how you can beta weight your portfolio delta’s (the change in value given a unit change of the underlying) to get an approximation for how your portfolio will change with respect to a movement in your benchmark (whether it be a market index or specific security).

Beta Weighting your Portfolio Read More »